[RAM] RAM Ratings affirms TNB's AAA/P1 issue ratings; outlook stable

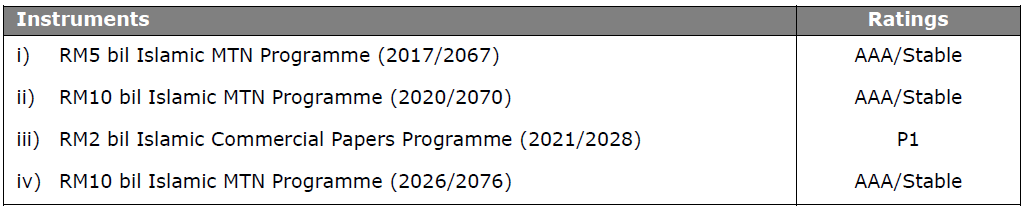

RAM Ratings has affirmed the AAA/Stable/P1 ratings of Tenaga Nasional Berhad’s (TNB or the Group) sukuk programmes (see table) in view of its strong credit profile, underpinned by its role as Malaysia’s largest electric utility.

The ratings reflect TNB’s dominant position in Peninsular Malaysia, where it maintains a near monopoly in transmission and distribution and owns more than half of installed generation capacity, supported by Single Buyer offtake arrangements. We view the extraordinary government support as very ‘highly likely’, if required, given the Group’s essential role in the provision of electricity as a public service.

For FY Dec 2025, pre-tax profit rose 6% y-o-y to RM6.18 bil, driven by the implementation of Regulatory Period 4, stronger commercial demand and lower borrowing costs despite higher debt. Working capital remained supported by healthy collections and the automatic fuel adjustment (AFA) mechanism.

A one-off tax payment following the Federal Court’s decision on Schedule 7B of the Income Tax Act 1967 and a heavier RM89.70 bil debt load (including lease liabilities which comprised about one-third) weakened leverage and cashflow metrics. The Group’s gearing increased to 1.69 times while funds from operations debt coverage (FFODC) declined to 0.14 times (end-December 2024: 1.66 times and 0.22 times respectively). The indicators, however, are still commensurate with the Group’s ratings, reflecting TNB’s regulated earnings profile and expectations of sovereign support.

We expect TNB’s performance to stay resilient, backed by the Incentive-Based Regulation framework and disciplined capital expenditure (capex) aligned with the National Energy Transition Roadmap. The Group’s regulated asset base grew 10% y-o-y to RM75.78 bil as at end-December 2025, underpinning future regulated revenue. Planned capex of RM18 bil for 2026 (FY Dec 2025: RM15.68 bil) is expected to be largely debt-funded. However, we project credit metrics to remain manageable with gearing at 1.74 times and FFODC at 0.19 times, supported by continued pass-through of fuel costs via the AFA mechanism and stable collections.

We assess TNB’s near-term exposure to heightened geopolitical risks in the Middle East as limited. Fuel supply for power generation remains adequate, with the majority of natural gas sourced domestically, while coal is secured through diversified long-term contracts primarily from Indonesia and Australia. Volatility in fuel prices may result in short-term timing differences in cashflow although we expect impact to be substantially mitigated by the AFA mechanism, which provides for timelier pass-through of fuel costs into end-user tariffs.

Analytical contacts

Liew Kar Ling

(603) 2708 8216

karling@ram.com.my

Chong Van Nee, CFA

(603) 2708 8210

vannee@ram.com.my

Media contact

Sakinah Arifin

(603) 2708 8212

sakinah@ram.com.my